Lamb Weston potato products

Potato Processor Lamb Weston Reports Fiscal First Quarter 2019 Results

Lamb Weston Holdings, Inc. (NYSE: LW) announced today its fiscal first quarter 2019 results.

Tom Werner, President and CEO:

“We’re pleased with our solid results in the first quarter, with each of our core business segments driving sales growth and expanding product contribution margins.”

“Our results continue to reflect the strong execution by our commercial, supply chain and support teams, as well as our ongoing commitment to invest in our production capacity, operating, sales and product innovation capabilities to support our customers’ growth, improve operating efficiency and execute on our strategies over the long term.”

“For the remainder of fiscal 2019, we continue to anticipate the operating environment in North America will remain generally favorable, with solid demand for frozen potato products and tight manufacturing capacity.”

“However, we expect that our European joint venture, Lamb Weston/Meijer, will face challenges arising from a poor potato crop.”

“Although it’s too early to determine the full impact of these challenges, we believe that Lamb Weston/Meijer’s pricing and cost reduction actions, along with opportunities in our North American and export businesses, enable us to remain on track to deliver on our fiscal 2019 targets.”

(Click to enlarge)

Summary of First Quarter FY 2019 Results

Q1 2019 Commentary

Net sales were $914.9 million, up 12 percent versus the year-ago period. Price/mix increased 8 percent due to pricing actions and favorable product and customer mix. Volume increased 4 percent, driven by growth in the Company’s Global and Retail segments.

Income from operations rose 11 percent to $152.6 million from the prior year period, which included $2.2 million of pre-tax costs related to the Company’s separation from Conagra Brands, Inc. (formerly ConAgra Foods, Inc., “Conagra”) on November 9, 2016.

Excluding this comparability item, income from operations grew $12.8 million, or 9 percent, driven by higher sales and gross profit. Gross profit increased $34.3 million due to favorable price/mix, volume growth, and supply chain efficiency savings.

This increase was partially offset by transportation, warehousing, input and manufacturing cost inflation, and higher depreciation expense primarily associated with the Company’s french fry production line in Richland, Washington, which started operating in the second quarter of fiscal 2018. In addition, gross profit included a $5.6 million loss related to unrealized mark-to-market adjustments and realized settlements associated with commodity hedging contracts in the current quarter, compared with a $3.2 million gain in the prior year period.

The rise in gross profit was partially offset by a $21.5 million increase in selling, general and administrative expenses (“SG&A”), excluding comparability items. The increase includes approximately $7 million of unfavorable foreign exchange, a $5 million increase in incentive compensation expense, primarily reflecting an increase in stock price and absolute shares outstanding, and a $3 million increase in advertising and promotional support. The remainder of the increase was largely driven by higher expenses related to information technology services and infrastructure, as well as investments in the Company’s sales, marketing and operating capabilities.

Adjusted EBITDA including unconsolidated joint ventures(1) was $212.9 million, up 11 percent versus the prior year quarter, primarily due to growth in income from operations.

Diluted EPS increased $0.17, or 30 percent, to $0.73, while Adjusted Diluted EPS(1) increased $0.16, or 28 percent, to $0.73. A lower U.S. corporate tax rate related to the U.S. Tax Cuts and Jobs Act (the “Tax Act”) increased Diluted EPS $0.10. The remaining increase reflects growth in income from operations.

The Company’s effective tax rate(2) was 23.5 percent in the first quarter of fiscal 2019, versus 33.3 percent in the prior year period. The lower rate in the first quarter of fiscal 2019 is attributable to the effects of the Tax Act enacted in December 2017.

Full Financial Release

For the full financial release, including additional details, the outlook for the remainder of 2019, as well as the explanations of the notes, we refer to the Lamb Weston Holdings websiteQ1 2019 Segment Highlights

Global Segment Summary

(Click to enlarge)

Net sales for the Global segment, which is comprised of the top 100 North American based restaurant chain customers as well as the Company’s international business, increased to $466.8 million, up 13 percent compared to the prior year period.Price/mix increased 8 percent, reflecting the carryover impact of pricing actions taken in the prior year as well as improvement in customer and product mix. Volume increased 5 percent, driven by the benefit of limited time product offerings and growth in sales to strategic customers in the U.S. and key international markets.

Global segment product contribution margin(1) increased to $94.5 million, up 27 percent compared to the prior year period. Favorable price/mix and volume growth drove the increase, which was partially offset by transportation, warehousing, input and manufacturing cost inflation, as well as higher depreciation expense primarily associated with the Richland production line.

Foodservice Segment Summary

(Click to enlarge)

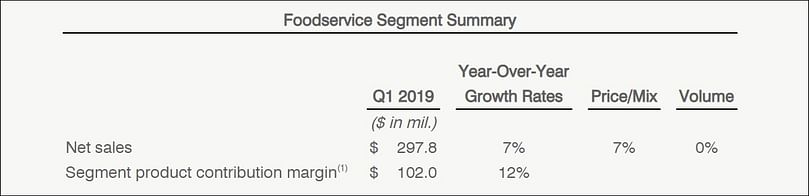

Net sales for the Foodservice segment, which services North American foodservice distributors and restaurant chains outside the top 100 North American based restaurant chain customers, increased to $297.8 million, up 7 percent compared to the prior year period.Price/mix increased 7 percent, reflecting carryover impact of pricing actions taken in the prior year as well as improvement in customer and product mix. Volume declined nominally as growth in sales of higher-margin Lamb Weston-branded and operator-labeled products largely offset the loss of some lower-margin, distributor-label product volumes.

Foodservice segment product contribution margin(1) increased to $102.0 million, up 12 percent compared to the prior year period, driven by favorable price/mix, partially offset by transportation, warehousing, input and manufacturing cost inflation, as well as higher depreciation expense primarily associated with the Richland production line.

Retail Segment Summary

(Click to enlarge)

Net sales for the Retail segment, which includes sales of branded and private label products to grocery, mass merchant and club customers in North America, increased to $116.2 million, up 26 percent compared to the prior year period.Price/mix increased 13 percent, due to higher prices across the private label and branded portfolios, as well as improved mix. Volume increased 13 percent, primarily driven by distribution gains of Grown in Idaho and other branded products.

Retail segment product contribution margin(1) increased to $22.7 million, up 38 percent compared to the prior year period, due to higher price/mix, volume and lower trade expense. The increase was partially offset by increased advertising and promotional support, as well as transportation, warehousing, input and manufacturing cost inflation.

Outlook

For fiscal 2019, the Company continues to expect:

- Net sales to grow mid-single digits, with price/mix higher in the first half of fiscal 2019 versus the second half of the year, reflecting the carryover impact of customer contract pricing structures that took effect beginning in the second half of fiscal 2018.

- Adjusted EBITDA including unconsolidated joint ventures(1) in the range of $860 million to $870 million. The Company continues to expect the rate of gross profit dollar growth to be at least in line with net sales growth.

The Company also continues to expect to incur significantly higher SG&A as it invests to upgrade its information systems and enterprise resource planning infrastructure, as well as sales, marketing, innovation, operations and other functional capabilities, designed to drive operating efficiencies and support future growth.

In addition, this range includes the impact of the Company exercising its contractual right to purchase the remaining 50.01% equity interest in its joint venture, Lamb Weston BSW, LLC, that it currently does not own (the “call option”). The Company has provided notice to exercise the call option, and expects to consummate the transaction as soon as practicable.

- Total interest expense to be approximately $110 million.

- An effective tax rate(2) of approximately 24 percent.

- Cash used for capital expenditures of approximately $360 million, excluding acquisitions, of which approximately $200 million is related to completing the construction of the Company’s 300 million pound french fry production line in Hermiston, Oregon, which is expected to be operational in May 2019.

- Total depreciation and amortization expense of approximately $150 million.

¿Te gustaría recibir noticias como esta por correo electrónico? ¡Únete y suscríbete!

Get the latest potato industry news straight to your WhatsApp. Join the PotatoPro WhatsApp Community!

Empresa Destacada

Related News

Diciembre 17, 2025

Lamb Weston’s First Retail Move into Southeast Asia Begins in Singapore

Lamb Weston entered Southeast Asia retail via Singapore, using it as a trend-setting test market. The company launched four oven- and air-fryer–ready fry SKUs, tailored to Asian habits, before planned expansion to Malaysia and beyond.

Diciembre 13, 2025

International Potato Center and HyFarm form strategic partnership to advance processing-grade potato sector in India

The International Potato Center (CIP) and HyFarm, the agri-business unit of HyFun Foods, have announced a strategic partnership to advance India’s processing-grade potato sector through scientific collaboration, technology exchange, and farmer-focused innovation.

Diciembre 08, 2025

McCain and Cargill strengthen partnership to drive sustainable frozen food growth in India

McCain Foods and Cargill are deepening their long-standing collaboration to drive innovation and sustainability in Indias frozen food category.Latest News

Contenido Patrocinado

Contenido Patrocinado

Contenido Patrocinado

Contenido Patrocinado