September marked the fourth consecutive monthly increase in the FAO Food Price Index

September marked the fourth consecutive monthly increase in the FAO Food Price Index

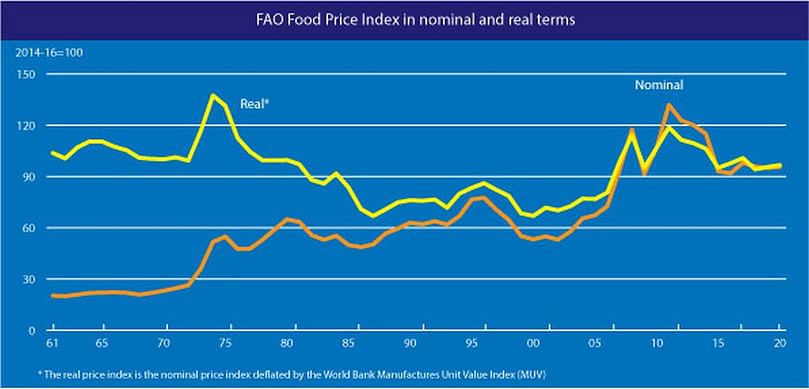

The FAO Food Price Index* (FFPI) averaged 97.9 points in September 2020, up 2.0 points (2.1 percent) from August and now 4.6 points (5.0 percent) higher than its value a year ago. The September value, the highest since February 2020, represented the fourth consecutive monthly increase.

Much firmer prices of vegetable oils and cereals were behind the latest rise in the FFPI. By contrast, prices of dairy products remained generally stable, while those of sugar and meat retreated from their August levels.

The FAO Cereal Price Index averaged 104.0 points in September, up 5.0 points (5.1 percent) from August and as much as 12.5 points (13.6 percent) above its value in the corresponding month last year. The September rise marked the third month of consecutive increase.

Reflecting brisk trade activity amidst increased concerns over production prospects in the southern hemisphere and dry conditions adversely affecting winter wheat sowings in many parts of Europe, wheat prices rose sharply in September.

International maize prices exhibited a notable surge as well, responding to cuts in production prospects, especially in the EU, and the expectation of a significant drop in supplies in the United States of America, following the downward revision of the country’s maize carryovers from the previous season.

Strong import demand from China kept sorghum prices on the rise for a third consecutive month, while international rice prices subsided by 1.4 percent, as 2020 crops entered or approached the harvesting stage in northern hemisphere suppliers, while fresh demand slowed.

The FAO Vegetable Oil Price Index averaged 104.6 points in September, up 5.9 points (or 6.0 percent) from August and marking an eight-month high. The further increase of the index mainly resulted from rising palm, sunflowerseed and soy oil quotations.

International palm oil prices rose markedly for the fourth consecutive month, tied to fresh global import demand as well as lower than expected inventory levels in Malaysia and uncertainties regarding the pace of production in Southeast Asia in the coming months.

At the same time, international sunflower oil prices increased sharply in September, primarily fuelled by deteriorating crop prospects in the Black Sea region.

As for soyoil, international prices continued rising, supported by the slow pace of crushings in South America and firm demand from the biodiesel industry in the United States of America.

The FAO Dairy Price Index averaged 102.2 points in September, almost unchanged from August and up 2.5 points (2.5 percent) from the corresponding month last year. Moderate increases in price quotations for butter, cheese and skim milk powder (SMP) were offset by a fall in those of whole milk powder (WMP), resulting in a nearly stable index in September.

Butter prices increased due to high demand for near-term deliveries and reduced processing in Europe, while cheese quotations rose slightly, reflecting a rise in import demand, coupled with an expanded internal demand in Europe despite continued weakness in food services sales.

Quotations for SMP rose too, resulting from somewhat tight supplies in Europe, where milk production is seasonally declining. By contrast, WMP prices fell, as import demand eased, especially from the Middle East, amid near-peak seasonal production in Oceania.

The FAO Meat Price Index** averaged 91.6 points in September, down slightly (0.9 percent) from August, continuing the general declining trend observed since January this year. Year-on-year, the index is down 9.5 points (9.4 percent) from its value in the corresponding month last year.

In September, quotations for pig meat fell, partly influenced by China's decision to impose a ban on imports from Germany following the detection of African swine fever (ASF) among wild boars, while ovine meat prices waned on high seasonal supplies from Australia.

By contrast, quotations for poultry meat rose, underpinned by the fast pace of international sales and limited exportable supplies from Brazil.

Bovine meat prices remained stable, as an increase in the quotations of Brazilian products was nearly offset by a decline in those from Australia, largely reflecting the underlying import demand conditions facing each market.

The FAO Sugar Price Index averaged 79.0 points in September, down 2.1 points (2.6 percent) from August. The decline in international sugar prices was mainly in reaction to expectations of a global sugar production surplus for the new 2020/2021 season.

The latest indications point to significant production recovery in India, the world's second largest sugar producer, as well as a strong output in Brazil, the world's largest exporter, following the decline registered last season.

Furthermore, the persisting weakness of the Brazilian Real against the United States dollar contributed to lowering world sugar prices.

* Effective July 2020, the price coverage of the FFPI has been expanded and its base period revised to 2014-2016. For more details on this revision, please see the feature article of the June 2020 issue of the Food Outlook.

** Unlike for other commodity groups, most prices utilized in the calculation of the FAO Meat Price Index are not available when the FAO Food Price Index is computed and published; therefore, the value of the Meat Price Index for the most recent months is derived from a mixture of projected and observed prices. This can, at times, require significant revisions in the final value of the FAO Meat Price Index which could in turn influence the value of the FAO Food Price Index.

Like to receive news like this by email? Join and Subscribe!

NEW! Join Our BlueSky Channel for regular updates!

Highlighted Company

")

Related News

February 19, 2025

KFC corporate offices are leaving Louisville, 100 jobs impacted

January 31, 2025

Convenience Stores Evolve to Become True Food Destinations

October 28, 2024

Himalaya Food International Limited: 60,000 TPA French Fry Plant Set to Launch by March 2025

Sponsored Content

Latest News

Sponsored Content

Sponsored Content

Sponsored Content

Sponsored Content

Sponsored Content